Posted on Tuesday, 13th February 2018 by Dennis Damp

Print This Post

Print This Post

What a ride the market has taken us on since my last article that talked about ways to preserve your retirement account balances during downturns. The DOW reached a high of 26,616 and the S&P 2,872 before this latest 10% downward draft.

Markets Trend Upward

The important fact is that over time, the market inevitably trends upward according to a recent Market Watch article. Anyone that is employed, in their mid to late career, generally have time on their side and will recover from a downturn if they stay invested. It’s the ones that panic and sell that suffer the consequences and end up losing a good portion of their investments. You can soften the blow by holding a conservative mix of stock, ETF, and bond funds as you approach retirement and rebalance each year.

Typically, those approaching or in retirement would have anywhere from 40% to 70% of their retirement accounts in bond funds, cash or individual bonds such as U.S. Treasuries. The mix depends on many factors including how much risk you can tolerate and more importantly how soon you will need the money to live on.

A market correction according to the article Stock Market Corrections Versus Crashes And How to Protect Yourself is “when the market falls 10 percent from its 52-week high. Wise investors welcome it. A pullback allows the market to consolidate before going toward higher highs. Each of the bull markets in the last 40 years has had corrections. It’s a natural part of the market cycle. Corrections can occur in any asset class.” A bear market is when the price of an investment falls over time. It occurs when prices drop 20 percent or more from their 52-week high.

Bear Markets and Recessions

A bear market can lead to a recession which is defined by Investopedia as, “A significant decline in activity across the economy, lasting longer than a few months. The technical indicator of a recession is two consecutive quarters of negative economic growth as measured by a country’s gross domestic product (GDP), although the National Bureau of Economic Research (NBER) does not necessarily need to see this occur to call a recession.”

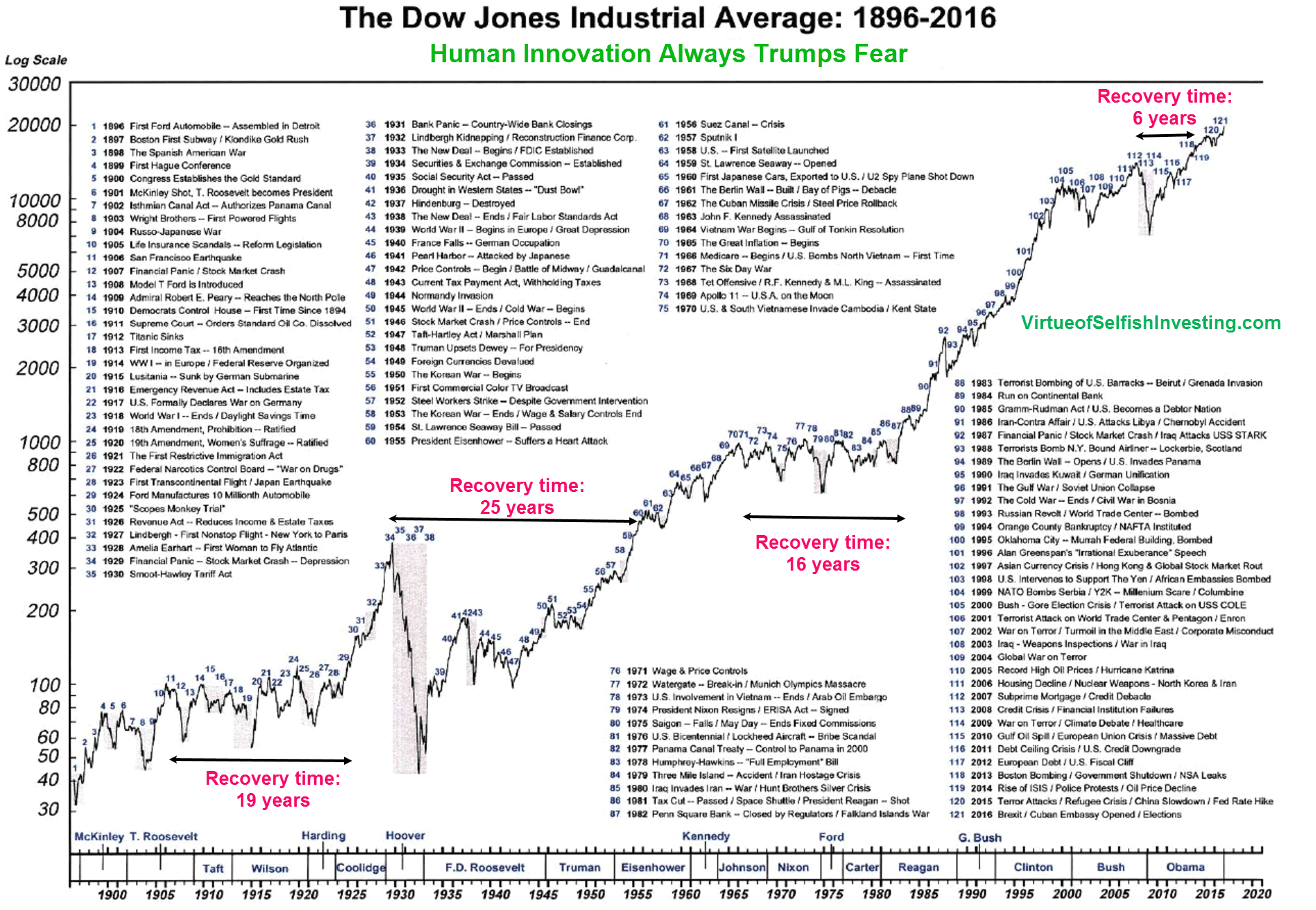

The risk for retirees and those approaching retirement is the recovery periods that are listed in the Dow charts. A stock market recovery is a period of increasing business activity signaling the end of a recession. When correlated to stock market returns, from my perspective, it is the time that it takes for the DOW and S&P to exceed a previous market high and continue on their upward progression.

{kind=link}

Over the past 120 years there has been many recessions and of course the great depression that started in 1929. From the early 1900s on there have been four major recessions with the longest recovery period from 1929 to 1955, 25 years. The average recovery period was 16.5 years! The shortest recovery period lasted only six years from 2009 to 2015. What most of us have experienced since 1985 are bull markets interrupted with one recession running six years from 2009 to 2015. Yet, the most recent recession always seems so much worse than earlier periods since it is fresh on our minds.

What does all of this really mean? There isn’t a short answer to this question and I don’t pretend to have all of the answers. I’m just a concerned and interested investor that is retired and wants to protect what I worked a life time to accumulate.

Caution When Approaching Retirement

Those approaching retirement and retirees don’t have time on their side to whether a major recession and the subsequent recovery. Life is finite and even though we may think we will live forever reality and age catches up with us. You never know what lies ahead and can only prepare as best we can to stay on top of things.

Even though corrections can last a long time individual funds and stocks recover at different intervals. Recoveries are typically referenced to a market index like the S&P that is comprised of the top 500 American companies. For example, if you would have had 100% of your non TSP investments in the Vanguard Wellesley Income Fund (VWINX) before the last bear market started in 2008 your investment would have only decreased approximately 9% compared to a more than 50% drop in the DOW & S&P indexes and you would have recovered all of your losses in less than a year!

The VWELX fund is a conservative mutual fund rated 5 Stars by Morningstar, yields 2.84%, and is comprised of roughly 60% bonds and 40% stocks. The average annual gain of this fund since its inception in 1970 is 9.82% and it only charges a .22% annual fee to manage the fund. The fund’s recent 10 year average annual return is 6.94%.

Conversely, had you had 100% of your private accounts invested in an S&P 500 indexed fund or invested all of your TSP account in the C Fund just before the last recession in 2008 you would have experienced more than a 50% drop in value. It would have taken you 5 years, until 2013, to recover your losses. Can you wait 5 years or longer to recover your losses?

I use the Wellesley Income Fund in my private sector brokerage accounts as an anchor to minimize market volatility. Another excellent Vanguard fund is their Wellington Fund (VWELX) that was founded in 1929! It is what they call a balanced fund or an all-in-one fund that invests 60% in stocks and 40% in bonds, rated 5 stars, and only charges a .22% annual management fee. The yield is 2.5%. If you invest $50,000 in the fund the management fee drops to .16% for their VWENX Admiral shares. This fund dropped 22% in 2008 and recovered eighteen months later to its previous high. Currently the Wellington Fund can only be purchased through a Vanguard brokerage account. The Wellesley fund can be purchased through most brokerage houses.

Summary

If you are approaching retirement or retired now, it makes sense to have a balanced account consisting of high quality mutual funds or ETFs that invest in stocks and bonds. The higher percentage of bonds and cash in your portfolio the more conservative and less volatile in general. However, you must be cautious with bonds as well. That’s why I lean towards managed funds like the two I mention in this article, where their researchers constantly monitor market conditions and adjust their stock and bond holdings accordingly.

Related Articles

- Preserving Your TSP & Other Retirement Account Assets

- The TSP Advantage (Should I Stay or Go)

- Survivor’s Beware – The TSP Trap

- TSP Survivor Withdrawal Options

Helpful Retirement Planning Tools / Resources

Distribute these FREE tools to others that are planning their retirement

- TSP Information

- Retirement Planning Guide

- Master Retiree Contact List (Important contact numbers and information)

- 2018 Leave and Schedule Chart (Excel chart tracks all leave balances. Use this chart to set target retirement dates.)

- Annuity Calculator (FREE Excel chart estimates annuity growth)

- The TSP Government Website – www.tsp.gov

Disclaimer: Opinions expressed herein by the author are not an investment or benefit recommendation and are not meant to be relied upon in investment or benefit decisions. The author is not acting in an investment, tax, legal, benefit, or any other advisory capacity. This is not an investment or benefit research report. The author’s opinions expressed herein address only select aspects of various federal benefits and potential investment in securities of the TSP and companies mentioned and cannot be a substitute for comprehensive investment analysis. Any analysis presented herein is illustrative in nature, limited in scope, based on an incomplete set of information, and has limitations to its accuracy.

The author recommends that retirees, potential and existing investors conduct thorough investment and benefit research of their own, including detailed review of OPM guidance for benefit issues and for investments the companies’ SEC filings, and consult a qualified investment adviser. The information upon which this material is based was obtained from sources believed to be reliable, but has not been independently verified. Therefore, the author cannot guarantee its accuracy. Any opinions or estimates constitute the author’s best judgment as of the date of publication, and are subject to change without notice. The author explicitly disclaims any liability that may arise from the use of this material.

Last 5 posts by Dennis Damp

- Retirement Planning Assistance – Finding Help (2025 Update) - July 17th, 2025

- Bits and Pieces – Updates, and Subscriber Feedback - July 11th, 2025

- Social Security Tax Relief for Millions of Senior Citizens - July 4th, 2025

- Apply for Retirement on OPM’s Online Application Service - June 27th, 2025

- New Retirement Application Portal Launched - June 20th, 2025

- 2026 COLA Estimates & Retirement Processing Update - June 12th, 2025

- Electronic Official Personnel Folder Platform Launched - June 5th, 2025

- Electronic Retirement Application Submissions - May 30th, 2025

- Powerless, Keeping the Lights On - May 22nd, 2025

- Request Your 2025 Retirement Benefits Booklet from OPM - May 16th, 2025

- Projected Annuity Calculator Updates for FERS and CSRS - May 9th, 2025

- Hiring Freeze, Schedule F, and Social Security Benefits - April 25th, 2025

Tags: Balanced Funds, Bear Markets, Market Volatility, Recessions

Posted in FINANCE / TIP, LIFESTYLE / TRAVEL, RETIREMENT CONCERNS, SOCIAL SECURITY / MEDICARE, SURVIVOR INFORMATION | Comments (0)

Print This Post