Posted on Sunday, 28th February 2021 by Dennis Damp

Print This Post

Print This Post

I’m often astonished after performing a due diligence update on my family’s state of affairs. You too will find reason to pause after putting pen to paper and discovering where you and your family stand financially. Not only your current status, but what a surviving spouse and heirs will have to live on when the inevitable happens. This process applies to anyone at all life stages.

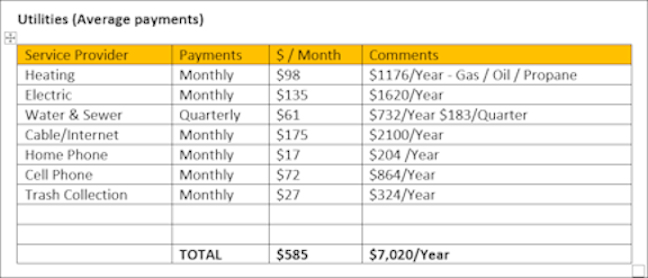

The forms I developed break expenses down to utilities, other, loans and payments, taxes (real estate and income), insurance, living, and second home costs compared to total income.

Many ponder where their money went after completing their income taxes! After updating these tables, I know exactly where it has disappeared to and the one word that comes to mind is TAXES: income, real estate, sales, gas tax, and many others that are hidden below the surface where government hopes we never discover just how pervasive they really are.

I’m not complaining, where would we be without the services and benefits taxes provide. However, they can become onerous and there are ways to reduce the burden if necessary, through prudent review and analysis. For example, Pennsylvania real estate taxes are extremely high. You can downsize and pay less or move out of state. South Carolina’s real estate taxes are a fraction of what we pay in Pennsylvania. It isn’t just taxes, costs across the board are rising; have you looked at your utility bills including cable and cell phone charges lately?

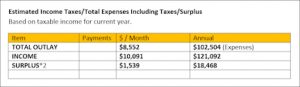

You will find a downloadable Microsoft Word and PDF document in this article that you can use to determine your financial health and what a surviving spouse will have to live on when the time comes. Use the example I prepared to review the process and methods used. The example depicts a retired couple with a gross income of $121,092 from all sources: annuities, social security, 401Ks, interest, dividends, salary, and capital gains if warranted. This process works just as well for those still working. The end result highlights areas that need attention such as excessive expenses in one category or another. It also identifies potential shortfalls; where your income is not quite sufficient to maintain your lifestyle, excessive debts, and the need to consolidate and compromise. When you sit down with your significant other to review the analysis, be prepared for the surprised looks and awestruck behavior. “So that’s where all of our money is going” or “What the hell is this!” If the retired couple in the sample paid off their mortgage before retiring their post retirement finances would improve considerably.

Worksheets

- Sample Worksheet (Word DOC)

- Worksheet (PDF Version) Fill in with pen or pencil

Replace the amounts in the word document example with your own to complete the analysis. You can add and delete rows using Word’s table properties. I also included a PDF with all amounts removed for those who prefer to fill in the document with pen or pencil.

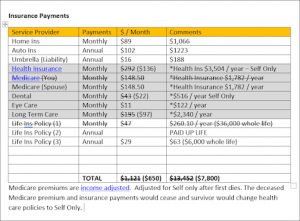

Finally, determine what your spouse or significant other will have when their partner passes. Line out the expenses for the deceased spouse or partner, as annotated in the following table, and add the new amount in parenthesis such as the lower cost for FEGLI “Self Only” premiums, etc. Then transfer your new calculations to the Expense Summary table. Many entries will change such as the reduced survivor’s annuity, the maximum survivor’s annuity is 55% of the annuitant’s full benefit for CSRS and 50% for FERS.

I used this online Income tax calculator to determine the federal income taxes owed for this example. Use this calculator to determine what taxes you can expect for your anticipated retirement income. Remember that most of your annuity is taxed and if you are over certain income limits eighty percent of your Social Security payments are subject to income tax. Also, be aware that Medicare premium are income adjusted and range from a low of $148.50 per person for couples filing a joint tax return with incomes of $178,000 or less to a high of $504 per couples earning $750,000 and above! Single filers pay the lowest rate if their income is $88,000 or less.

The final document table on page 4 compares Total Income to Expenses. You would modify this table as noted above to determine the financial health of a surviving spouse. It also helps to complete a Survivor’s Checklist long before it is needed. Keep this free fillable PDF checklist readily available, it includes necessary benefit contact information for retirees.

I was never a boy scout, but learned early in life it’s always best to be prepared. It may take several hours or more to determine your costs for each entry and income figures but I believe you will be glad you did. Once you see where you are at, you can effectively plan on getting to where you want to go. My next article will talk about preparing a comprehensive caretaker / survivor file with recommended shortcuts, and how to prepare individual account instruction sheets.

Request a Federal Retirement Report

Retirement planning specialists provide a comprehensive Federal Retirement Report™ including annuity projections, expenditures verses income, with a complete benefits analysis. This comprehensive 27-page benefits summary will help you plan your retirement.

Request Your Personalized Federal Retirement Report™ Today

Find answers to your questions: The best time to retire, retirement income vs expenditures, FEGLI options and costs, TSP risks and withdrawal strategies, and other relevant topics. Determine what benefits to carry into retirement and their advantages. You will also have the opportunity to set up a personal one-on-one meeting with a CERTIFIED FINANCIAL PLANNER.

Helpful Retirement Planning Tools

- Retirement Planning For Federal Employees & Annuitant

- GS Pay Scales

- Budget Work Sheet

- Medicare Guide

- Social Security Guide

- Master Retiree Contact List (Important contact numbers and information)

- 2021 Leave and Schedule Chart (Use this chart to set target retirement dates.)

- Annuity Calculator (FREE Excel chart estimates annuity growth)

Disclaimer: The information provided may not cover all aspect of unique or special circumstances, federal regulations, medical procedures, and benefit information are subject to change. To ensure the accuracy of this information, contact relevant parties for assistance including OPM’s retirement center. Over time, various dynamic economic factors relied upon as a basis for this article may change. The advice and strategies contained herein may not be suitable for your situation and this service is not affiliated with OPM or any federal entity. You should consult with a financial, medical or human resource professional where appropriate. Neither the publisher or author shall be liable for any loss or any other commercial damages, including but not limited to special, incidental, consequential, or other damages.

Last 5 posts by Dennis Damp

- Protecting Your Retirement Nest Egg – Fixed Income Update - February 26th, 2026

- Your 2026 Step-by-Step Federal Retirement Planning Guide - February 19th, 2026

- Online Retirement Application (ORA) Update - February 13th, 2026

- The End to the Silver Script Madness – News Flash - February 7th, 2026

- Reflections 2025 – Marvin Gaye (What’s Going On) - January 30th, 2026

- The Federal Workforce Data (FWD) Release – OPM Update - January 23rd, 2026

- Savings Bond Calculator & Treasury Direct Inefficiencies! - January 15th, 2026

- Tax Forms Availability – What to Expect This Year - January 9th, 2026

- The 2026 Landscape: What to Expect and Outlook - January 1st, 2026

- Long Term Care Insurance - Future Purchase Option - December 12th, 2025

- Open Season Coming to a Close – Last-Minute Checkup - December 2nd, 2025

- I Rolled Over My TSP Account to an IRA – Should You? - November 21st, 2025

Posted in ANNUITIES / ELIGIBILITY, BENEFITS / INSURANCE, ESTATE PLANNING, FINANCE / TIP, RETIREMENT CONCERNS, SOCIAL SECURITY / MEDICARE, SURVIVOR INFORMATION | Comments (0)

Print This Post